Watching mortgage rates climb past 6% while sitting on a 2.5% rate feels like being stuck. Moving means giving up that low rate forever — and for millions of homeowners right now, that trade-off simply does not make financial sense. A portable mortgage is the solution that lets you take your existing rate with you when you move, and this guide covers everything you need to know about how it works, where it exists, and what your real options are today.

The lock-in effect is real, and it is keeping homeowners frozen in place across the country. By the end of this article, you will understand exactly how mortgage portability works, why it is gaining serious attention in the US, and what steps you can take right now regardless of where the policy debate lands.

What Is a Portable Mortgage?

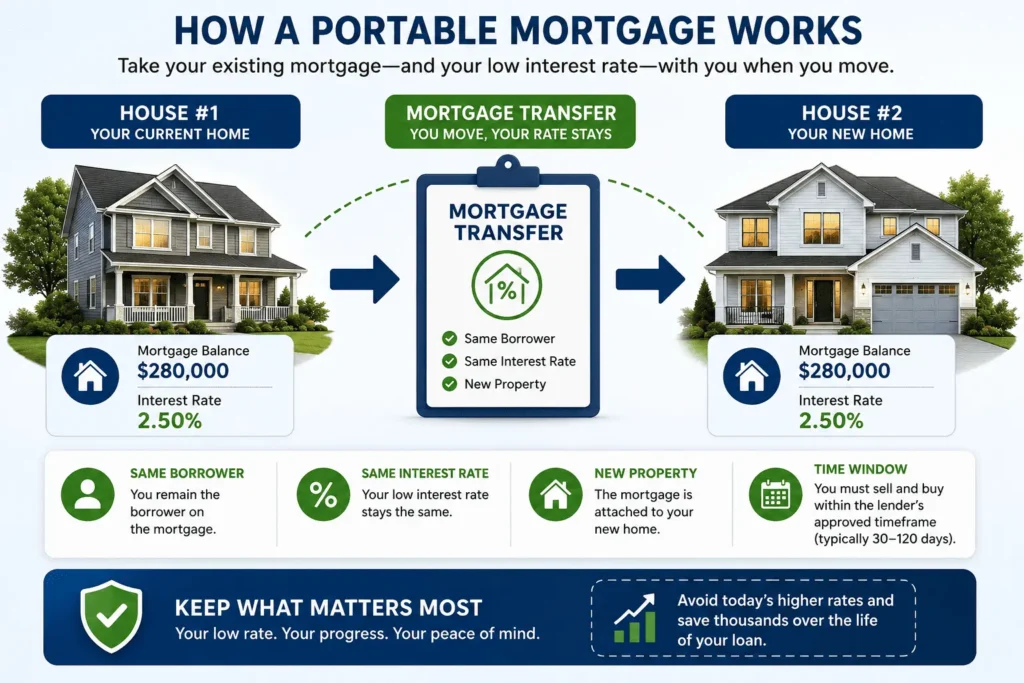

A portable mortgage is a home loan you can transfer from one property to another when you move. Instead of paying off your existing loan at the point of sale, you carry that same mortgage — including the interest rate, remaining balance, and loan term — over to your next home.

The borrower stays the same throughout the process. Only the property attached to the loan changes. This is the core portable mortgage definition that separates it from every other mortgage product on the market.

It works differently than an assumable mortgage, which is worth clarifying early. With an assumable mortgage, a buyer takes over a seller’s existing loan. With a portable mortgage, the seller keeps the loan and moves it to their next purchase. Same borrower, new address, same terms.

For someone locked into a 3% rate today, this is not just convenient — it is worth tens of thousands of dollars over the life of the loan.

How Does a Portable Mortgage Work?

The process starts when you decide to sell your current home and buy a new one. Your lender requires you to complete both transactions within an approved time window — typically 30 to 120 days depending on the lender’s policy. Outside that window, the port is cancelled and you lose the ability to transfer the loan.

Before the transfer is approved, your lender re-evaluates your financial situation. Your income, credit score, and debt levels are all reviewed again. The new property also has to meet the lender’s requirements for value and condition. Re-qualification is not optional — even though it is your own existing loan, approval is not guaranteed.

One critical detail most people overlook: you cannot reload your mortgage principal back to its original amount at your old rate. If you started with a $350,000 loan and have paid it down to $240,000, only that $240,000 transfers. You cannot top it back up to $350,000 at the lower rate.

How the numbers actually work out depends on whether your new home costs less or more than your current one.

Porting to a Less Expensive Home

This is the straightforward scenario. Your sale proceeds reduce your outstanding balance to fit the new property’s value, and your existing rate continues on that lower balance.

Say you owe $260,000 at 3% and your new home costs $230,000. The extra $30,000 from the sale pays down the loan balance. You carry the remaining $230,000 forward at 3% with no new loan required and no new rate involved.

Your original loan term continues as if nothing changed. The amortization clock keeps running from where it left off, which means you are also paying down principal faster than someone starting a fresh 30-year loan.

This scenario is the cleanest version of porting — no blending, no complications, just your original deal on a new property.

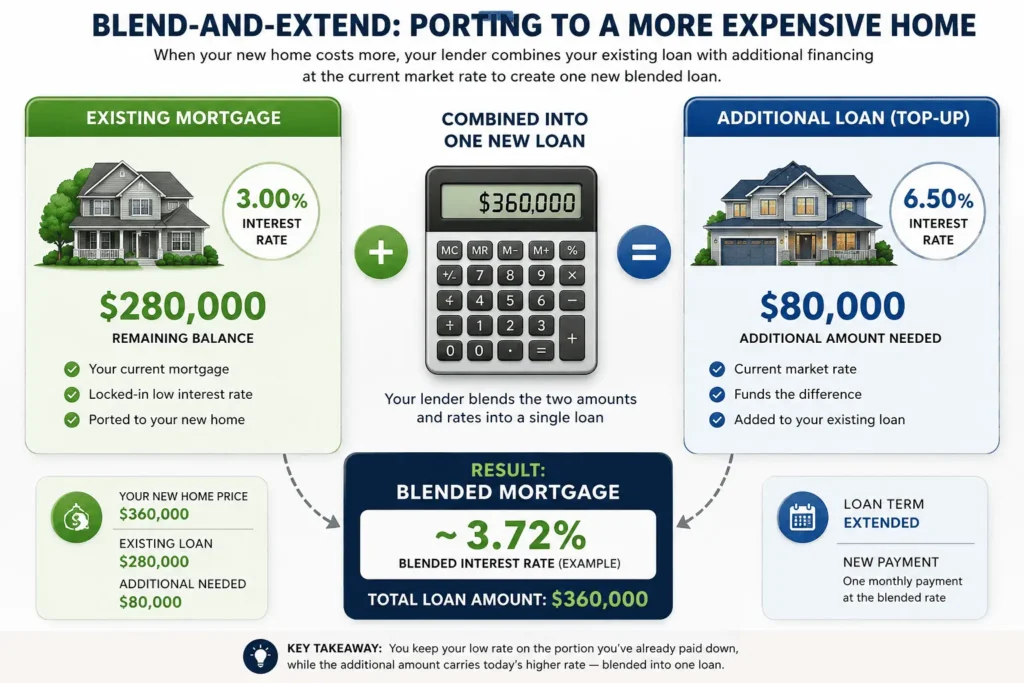

Porting to a More Expensive Home: How Blend-and-Extend Works

When your new home costs more than your existing mortgage balance covers, you need extra financing. Your lender handles this through a blend-and-extend arrangement — and this is where most articles stop explaining clearly.

Here is how it works with real numbers. You have $280,000 remaining on your mortgage at 3%. Your new home costs $360,000, so you need an additional $80,000. Your lender charges the current market rate — say 6.5% — on that $80,000 top-up. They then calculate a weighted average across the full $360,000 loan amount.

The blended rate lands somewhere between 3% and 6.5% — better than taking a fully new mortgage at today’s rates, but not as good as keeping your entire loan at 3%. The exact number depends on the size of each portion and your lender’s specific calculation method.

Your loan term also gets extended to accommodate the new financing, which is where the “extend” part of blend-and-extend comes from. The result is one single monthly payment at the blended rate covering the full loan amount.

Where Are Portable Mortgages Available Today?

This type of loan is a standard product in Canada and the United Kingdom. Both countries have offered them for years — not as a special feature but as a normal part of how their mortgage markets operate.

The reason portability works in those countries comes down to loan structure. Mortgage terms in Canada and the UK run two to five years, not 15 or 30 years like in the US. Borrowers renew and renegotiate at the end of each short term, which makes building portability into the contract far simpler.

How Portable Mortgages Work in Canada

Canadian lenders have included portability as a standard mortgage feature for decades. When a borrower wants to move, they sell their current home and purchase the new one within the lender-approved window — usually 30 to 120 days. The lender transfers the existing loan to the new property after re-qualifying the borrower and reviewing the new home.

Canadian mortgages also carry prepayment penalties, which makes porting especially attractive. Breaking a mortgage early to take out a new one can cost thousands in exit fees. Porting the loan sidesteps that cost entirely while preserving the existing rate and terms.

How Portable Mortgages Work in the UK

Most major UK lenders advertise portability as a benefit of their mortgage products, particularly during fixed-rate periods. The mechanics involve reapplying with your current lender for the new property — you keep your existing rate by staying with the same lender rather than switching.

UK portability is not automatic approval. The lender assesses your current financial situation at the time of the move. If your income has dropped or your debt has increased since your original application, the lender can decline the port even if you have been making payments without issue.

The main driver in the UK is avoiding early repayment charges. Fixed-rate periods there typically run two to five years, and breaking out of one early triggers significant penalties. Porting lets borrowers move homes without triggering those charges.

Why Portable Mortgages Are Getting Attention in the US

The numbers behind the US housing market explain why this conversation is happening now. More than half of American mortgage holders have rates at 4% or below. Around 80% are sitting below 6%. New mortgages today are being issued at roughly 6.5%.

That gap has a real dollar cost. The difference between a 4.4% rate and a 6.16% rate on a $400,000 home works out to approximately $350 per month. Across a full 30-year loan, that difference totals around $125,700. With that much money at stake, the decision to stay put rather than sell makes complete financial sense for millions of homeowners.

A working paper from the National Bureau of Economic Research found that rising rates reduced household mobility by 16% in 2022 and 2023, creating an estimated $20 billion in lost economic value. Homeowners are not moving to better jobs, better school districts, or better-suited homes because the financial penalty is too steep.

In November 2025, FHFA Director Bill Pulte publicly confirmed the agency is “actively evaluating” portable mortgages as a policy solution. The proposal sits alongside other ideas under review, including assumable mortgage expansion and longer loan terms. Nothing has been approved yet, but the fact that the FHFA is treating it as a serious option marks a real shift in how US housing policy discussions are moving.

Are Portable Mortgages Available in the United States?

No. As of 2026, it do not exist in the US mortgage market. No lender currently offers this product, and no federal program has been launched to make it available. The FHFA evaluation is ongoing, but there is no timeline for implementation.

The barriers are not just bureaucratic — they are structural. The way US mortgage lending is built makes portability genuinely difficult to introduce without rewriting significant parts of how the system works.

Why the US Mortgage System Makes Portability Difficult

US mortgage lending is built on securitization. Lenders bundle thousands of individual loans into mortgage-backed securities and sell them to investors. Every loan in that bundle is tied to a specific property — that property is the collateral that determines the risk and value of the security.

When a mortgage becomes portable, the collateral changes mid-loan. A security that was backed by a property in one state suddenly has a different property in a different state as its foundation. Investors who priced that security based on the original collateral now hold a different asset than what they purchased. That breaks the core logic of how MBS markets are priced and traded.

Beyond securitization, US mortgages are structured as closed-end contracts. Modifying one to allow porting requires a far more complex legal change than standard loan modifications. Regulation Z — the federal consumer credit disclosure law — adds another layer, since moving funds to a new property would likely trigger new disclosure and compliance requirements.

Canada and the UK do not face these same barriers because their lenders hold more loans on their own books rather than selling them into securities markets. The system architecture is fundamentally different, which is why portability developed naturally there and has not in the US.

Pros and Cons of Mortgage Portability

It solve a real problem — but only for a specific group of people. Understanding both sides gives you a clear picture of whether this product would actually help your situation.

Benefits:

- Keep your existing low interest rate when you move to a new home

- Avoid prepayment penalties and early exit fees on your current loan

- Pay down principal faster compared to restarting a fresh 30-year loan

- Save on loan origination fees and closing costs tied to new mortgage applications

- Gain freedom to move without the financial penalty of today’s higher rates

Limitations:

- Only existing homeowners with low locked-in rates benefit — everyone else faces the same market

- Re-qualification is required even though it is your own loan

- You cannot increase your principal back to the original amount at the lower rate

- The 30 to 120 day sell-and-buy window creates serious timing pressure

- Buying a more expensive home means a blended rate — not your full original rate on the whole amount

- Renters, first-time buyers, and homeowners without mortgages see no benefit at all

| Borrower Type | Does Portable Mortgage Help? |

|---|---|

| Homeowner with sub-4% rate | ✅ Yes — significant savings |

| Homeowner moving to cheaper home | ✅ Yes — clean transfer |

| Homeowner moving to pricier home | ⚠️ Partial — blended rate applies |

| First-time buyer | ❌ No — does not apply |

| Renter | ❌ No — no existing mortgage to port |

| Homeowner without a mortgage | ❌ No — nothing to transfer |

Alternatives to Porting Your Mortgage for US Homeowners

Since this option is not available in the US today, these are the real options that exist right now for homeowners trying to manage their rate situation.

Assumable Mortgages FHA, VA, and USDA loans are assumable — meaning a buyer can take over your existing mortgage including your low rate. This does not let you keep your rate on a new home, but it makes your current home more attractive to buyers and gives you stronger negotiating leverage on your sale price.

Mortgage Refinancing If rates drop in the future, refinancing lets you replace your current loan with a new one at a lower rate. It is the most straightforward long-term tool for managing your rate. Staying on top of your current loan through your servicer’s online tools — such as through a Freedom Mortgage payment login — keeps your existing account in good standing while you monitor the rate environment.

Temporary Rate Buydowns Some sellers are offering rate buydowns as a negotiating incentive. A buyer accepts today’s higher rate but gets a reduced rate for the first one to three years of the loan. It lowers the immediate payment burden while the broader market adjusts.

Bridge Loans A bridge loan lets you borrow against your current home’s equity to fund a new purchase before your existing home sells. It solves the timing gap but comes with higher short-term borrowing costs that need to be factored into the math.

Conclusion

A portable mortgage allows homeowners to carry their existing loan and low interest rate to a new property instead of starting over at today’s higher rates. This guide covered exactly how porting works, where it is available globally, why the US system has not adopted it yet, and what real alternatives exist for American homeowners right now. The financial case for portability is strong, and with the FHFA actively evaluating the concept, the landscape could shift. Until it does, knowing every tool available puts you in the best position to make a smart, informed move.

Frequently Asked Questions

Q1: What is a portable mortgage in simple terms?

A portable mortgage lets you move your existing home loan to a new property when you sell and buy again. You keep the same interest rate, remaining balance, and loan term. Only the property attached to the loan changes — the borrower and the deal stay exactly the same.

Q2: Who qualifies for a portable mortgage?

To qualify, you must have an existing mortgage with a portability clause, sell your current home, and buy a new one within your lender’s approved time window — usually 30 to 120 days. You also need to re-qualify based on your current income, credit score, and the new property’s value.

Q3: Does porting a mortgage save money?

Yes. Porting saves money in three ways — you keep your lower interest rate instead of borrowing at today’s higher rates, you avoid prepayment penalties on your existing loan, and you skip the origination fees that come with taking out a completely new mortgage from scratch.

Q4: What is the difference between a portable mortgage and refinancing?

Porting transfers your existing loan and rate to a new property without breaking your mortgage. Refinancing replaces your current loan with a new one, usually at a different rate. Porting preserves your original terms — refinancing creates entirely new loan terms based on current market conditions.

Q5: Can you port a mortgage to any home?

No. The new property must meet your lender’s requirements for value, condition, and location. Your lender approves or declines the transfer based on the new home’s assessment. If the property does not qualify under lender guidelines, the port is rejected even if your finances are in good standing.