Your mortgage payment feels heavy every single month. You have some extra cash sitting around and you are wondering if there is a smarter way to use it than just making an extra payment. Most homeowners never hear about recasting a mortgage until they stumble across it by accident — and when they do, it changes how they think about their loan completely.

This guide breaks down exactly what recasting mortgage is, how the process works from start to finish, who can qualify, and when it actually makes sense for your situation. By the end, you will know whether recasting is the right move for you or not.

What Does Recasting Mortgage Mean

Recasting mortgage means you make a large lump-sum payment toward your loan’s principal balance. Your lender then recalculates your monthly payment based on that new, lower balance. Your interest rate stays the same. Your loan term stays the same. Only your monthly payment goes down.

This process is also called re-amortization or a loan recast. It is not a new loan. You are simply restructuring how the remaining balance gets paid off. The lender builds a brand new amortization schedule based on what you still owe after your lump-sum payment. Every future monthly payment is now calculated against that lower balance — which means less interest charged every single month going forward.

Think of it this way. You owe $300,000 on your home. You pay $50,000 toward the principal. Your lender now recalculates your monthly payment based on a $250,000 balance at your same interest rate and same remaining term. Your payment drops — sometimes by hundreds of dollars per month.

A common question homeowners ask is whether a recast resets the life of the loan. It does not. Your loan term stays exactly where it was. If you had 22 years left before the recast, you still have 22 years left after. Only the monthly payment amount changes — nothing else.

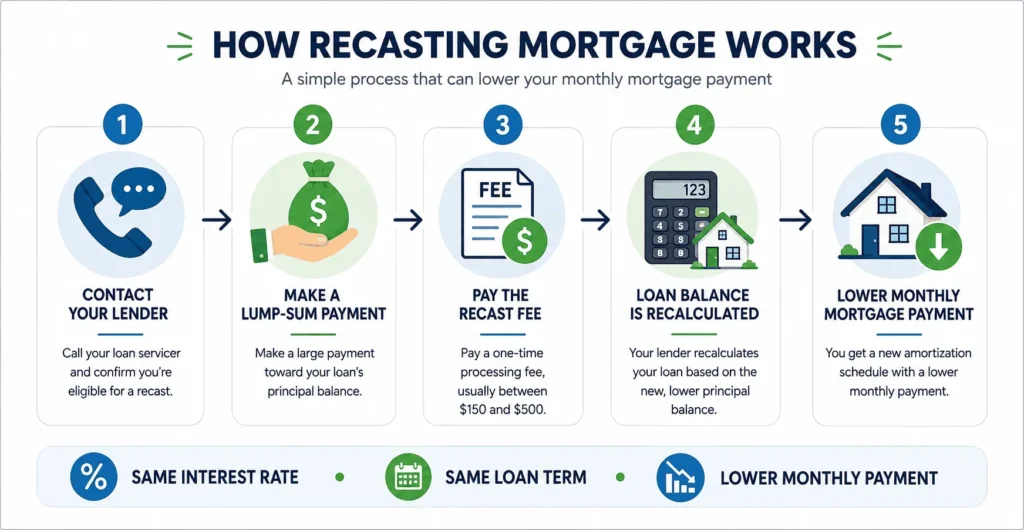

How Recasting Mortgage Works

The process is straightforward and does not require the paperwork nightmare that comes with refinancing. Here is how it works step by step.

Step 1 — Contact your lender first. Not every lender offers recasting. Call your loan servicer and ask if your loan is eligible. Get the minimum lump-sum requirement and the processing fee before you do anything else.

Step 2 — Make your lump-sum payment. Most lenders require a minimum of $5,000 to $10,000. Some require more. You make this payment directly toward your principal balance through your lender’s online portal or payment system.

Contact your lender first. Not every lender offers recasting. Call your loan servicer and ask if your loan is eligible. If your mortgage is serviced by Freedom Mortgage, you can access your account through the Freedom Mortgage login portal to review your loan details before requesting a recast.

Step 3 — Pay the recast fee. Lenders charge a processing fee that typically ranges from $150 to $500. This is a one-time cost and is far cheaper than refinancing closing costs which can run $3,000 to $6,000 or more.

Step 4 — Wait for your new schedule. The recast process takes 45 to 60 days to complete. Keep making your regular monthly payments during this time. Once processed, your lender sends you a new amortization schedule showing your lower payment going forward.

Before and After Recast — Real Numbers

| Detail | Before Recast | After Recast |

|---|---|---|

| Remaining Loan Balance | $300,000 | $250,000 |

| Interest Rate | 5.5% | 5.5% |

| Remaining Term | 25 years | 25 years |

| Monthly Payment (P&I) | $1,841 | $1,535 |

| Monthly Savings | — | $306 |

| Total Interest Saved | — | ~$36,700 |

A $50,000 lump-sum payment saves over $36,000 in total interest and drops the monthly payment by $306. The recast fee of $250 to $500 pays for itself in the very first month.

Who Qualifies for Mortgage Recasting

Not every homeowner can recast. Eligibility depends on your loan type, your lender’s rules, and your payment history.

Loan Types That Are Eligible

Conventional loans are the primary loan type that qualifies for recasting. These include loans backed by Fannie Mae and Freddie Mac. Most standard 30-year and 15-year fixed-rate conventional mortgages are eligible. Some adjustable-rate mortgages (ARMs) may also qualify depending on your lender’s policy — always confirm directly with your servicer.

Loan Types That Cannot Be Recast

Government-backed loans do not qualify for this process. This includes:

- FHA loans insured by the Federal Housing Administration

- VA loans guaranteed by the Department of Veterans Affairs

- USDA loans backed by the U.S. Department of Agriculture

- Most jumbo loans — though some lenders make exceptions, so it is worth asking

If you have one of these loan types and want lower payments, refinancing may be your best option instead.

Other Lender Requirements to Meet

Beyond loan type, lenders typically require the following:

- Your loan must be current — no missed or late payments

- You must meet the minimum lump-sum payment amount set by your lender

- Some lenders require a minimum amount of home equity before they approve a recast

- You must pay the processing fee at the time of the request

Requirements vary by lender. Always confirm the exact rules with your loan servicer before making any large payment.

Recasting Mortgage vs. Refinancing

These two options both lower your monthly payment but they work in completely different ways. Understanding the difference helps you pick the right one.

| Factor | Recasting | Refinancing |

|---|---|---|

| Interest Rate | Stays the same | Changes — could go up or down |

| Loan Term | Stays the same | Resets — usually to a new 30 years |

| Credit Check | Not required | Required |

| Home Appraisal | Not required | Usually required |

| Processing Time | 45 to 60 days | 30 to 60 days |

| Cost | $150 to $500 | $3,000 to $6,000+ |

| Lump Sum Required | Yes | No |

| Loan Type Eligibility | Conventional only | Most loan types |

Recasting mortgage makes more sense when you have a low interest rate you want to keep. Refinancing makes more sense when current rates are lower than your existing rate and you want to save on interest over the long term.

If you are comparing recasting and refinancing options through different lenders or mortgage channels, understanding how wholesale lending works can also be helpful. Borrowers researching broker-based loan services may find our guide on Freedom Wholesale Mortgage login useful for learning more about account access and loan management.

Recasting Mortgage vs. Making Extra Principal Payments

This is the comparison most articles skip — and it is one of the most important ones to understand.

When you make extra principal payments, your loan balance goes down. But your required monthly payment does not change. The benefit is that you pay off the loan faster and save on total interest. Your cash flow every month stays exactly the same.

When you recast, your loan balance goes down AND your required monthly payment drops. The benefit is immediate relief on your monthly budget. But your loan term stays the same — you do not pay off the loan any faster.

These two options serve different goals. Extra payments are for homeowners who want to be debt-free sooner. A recast is for homeowners who want more breathing room in their monthly budget right now. If cash flow is tight and you need that monthly savings, a recast is the better move. If your budget is fine and you just want to eliminate debt faster, extra payments win.

There is also a middle ground worth knowing. Some homeowners make extra payments consistently over time and then request a recast once they have built up enough principal reduction to qualify. This approach gives you the best of both — you reduce debt steadily and then lock in a lower payment when the time is right.

When Recasting Your Mortgage Makes the Most Sense

Recasting is not right for everyone. But in certain situations, it is one of the smartest financial moves a homeowner can make.

You Received a Windfall and Want Lower Payments

An inheritance, a large work bonus, proceeds from selling a previous home, or a life insurance payout — these are the most common reasons homeowners recast. Many homeowners find themselves buying a new home before their old one sells. Once that old home closes, they take those sale proceeds and apply them directly to the new mortgage through a recast. It cuts the monthly payment significantly without giving up the existing loan terms.

You Want to Remove Private Mortgage Insurance

If you put less than 20 percent down when you bought your home, you are likely paying private mortgage insurance (PMI) every month. PMI can cost $50 to $200 or more per month depending on your loan size. A large lump-sum payment during a recast can push your loan-to-value ratio below 80 percent. Once you cross that threshold, you can request PMI cancellation. This saves you money two ways — a lower principal balance and no more PMI premium.

After making a large principal payment, it is important to monitor your updated loan balance and monthly obligations. Borrowers with Freedom Mortgage can review these details through the Freedom Mortgage Payment Login portal while tracking their progress toward PMI removal.

You Have a Low Rate You Do Not Want to Lose

Many homeowners locked in rates at 3 percent or 4 percent in recent years. Refinancing today means giving up that rate for something much higher. A recast lets you lower your monthly payment while keeping your existing low rate completely intact. This is one of the strongest cases for recasting in a high-rate environment.

You Are Nearing Retirement

Heading into retirement on a fixed income means every dollar matters. A lower required monthly mortgage payment reduces your financial pressure significantly. Recasting before you retire gives you a predictable, lower payment without the credit scrutiny and costs of a full refinance.

When Recasting Is Not the Right Move

Recasting a mortgage is not always the answer. There are real situations where it makes little sense or could actually hurt you financially.

You plan to sell the home soon. If you are selling in the next one to two years, a recast does not give you enough time to recover the lump-sum payment through monthly savings. Your cash would be better kept liquid or used elsewhere.

Your rate is already high. If you locked in at a high interest rate, refinancing to a lower rate saves you far more money over time than a recast ever could. Do the math before committing a large payment.

You need the cash for emergencies. Draining your savings or emergency fund to recast is a risky move. Once you hand that money to your lender as a principal payment, it is tied up in your home equity. You cannot access it easily if something goes wrong.

The lump sum could earn more elsewhere. If your mortgage rate is low and the stock market or other investments are returning more, keeping the cash invested may be smarter than locking it into your home. Consider the opportunity cost before deciding.

The right call depends on your specific numbers. A homeowner with a 3 percent mortgage rate and solid investment options is in a very different position than someone with a 7 percent rate and no other place to grow their money. Always compare your mortgage interest rate against realistic returns before committing your lump sum to a recast. A quick conversation with a financial advisor can help you see which path actually puts more money in your pocket over time.

Conclusion

Recasting a mortgage is one of the most underused tools in a homeowner’s financial playbook. You now know exactly how the process works, who qualifies, what it costs, and when it makes the most sense for your situation. Whether you just sold a home, received a windfall, or simply want more breathing room in your monthly budget — a recast could be the move that changes your financial picture permanently. Talk to your loan servicer today, confirm your eligibility, and run the numbers before making your decision.

Frequently Asked Questions

What Is the Minimum Amount Needed to Recast a Mortgage?

Most lenders require a lump-sum payment of at least $5,000 to $10,000 to qualify for a recast. Some lenders set the minimum higher depending on your loan size and their internal policy. Always confirm the exact minimum with your loan servicer before making any payment toward your principal balance.

Does a Recast Affect Your Credit Score?

No, recasting does not affect your credit score at all. There is no credit check involved in the process. Your lender simply recalculates your monthly payment after you make the lump-sum payment. Because no new loan is created and no hard inquiry is made, your credit report remains completely untouched.

Does Recasting a Mortgage Make Sense if I Plan to Move in 5 Years?

It depends on how much you save monthly versus what you put in. If your recast saves $250 per month and you plan to stay 5 years, you recover $15,000 in savings from your lump-sum payment. Run that math against your specific numbers before deciding. If the break-even point is beyond your move date, skip the recast.

Does Recasting a Mortgage Affect My Home Equity?

No, recasting does not change your home equity directly. When you make a lump-sum payment to recast, your loan balance drops which means your equity increases by that same amount. The recast itself does not change your home’s market value — only your outstanding debt goes down.

Can You Recast Your Mortgage More Than Once?

Yes, there is no universal rule limiting how many times you can recast. Some lenders allow multiple recasts over the life of a loan while others may limit you to one or two. Each recast typically comes with its own processing fee of $150 to $500. Check your loan servicer’s specific policy before deciding.