You just found a new rate quote online and your stomach dropped a little. Maybe you searched RoundPoint Mortgage Rates last night and landed on pages full of old reviews with no real numbers anywhere. A lot of homeowners feel this same frustration when a loan servicer keeps its pricing behind a phone call instead of a webpage. That confusion is exactly what pushed you here.

This guide breaks down current RoundPoint Mortgage Rates by loan type, shows how they stack up against the national average, and walks you through the exact steps to lock in a stronger deal today. You will see real fee data, a lender comparison table, and a plain answer to whether this servicer fits your financial goals. No guesswork, just the numbers you came for.

RoundPoint Mortgage Rates

RoundPoint Mortgage Servicing LLC has been part of the home lending industry since 2007. The company mostly services existing home loans, but it also offers new purchase loans, refinance options, and home equity products. In 2023, Two Harbors Investment Corp acquired RoundPoint, which shifted some of its pricing and technology behind the scenes.

If you want the full picture of how RoundPoint handles logins, payments, and account access, our RoundPoint Mortgage guide covers those basics in detail. For rate shoppers, the biggest thing to know is this: RoundPoint does not publish live rates on its public site. You need to speak with a loan officer or start an application to see your personal number.

RoundPoint is licensed as a national mortgage servicer and lender, which means it follows the same federal disclosure rules as bigger banks. It holds an A+ rating with the Better Business Bureau, even though it is not accredited by that group. Homeowners who want a company with a long service history, rather than a brand new startup lender, often see this track record as a plus. Understanding this background helps you judge whether the company fits your comfort level before you request a quote.

Current RoundPoint Mortgage Rates by Loan Type

RoundPoint offers pricing across several common loan types. The table below shows typical rate ranges based on recent industry data and RoundPoint’s own origination patterns. Your exact number will depend on credit score, down payment, and property type.

| Loan Type | Typical Rate Range | Best For |

|---|---|---|

| 30-Year Fixed | 6.3% to 6.9% | Buyers who want stable payments |

| 15-Year Fixed | 5.6% to 6.1% | Owners who want to pay off faster |

| 5/1 ARM | 5.9% to 6.5% | Short-term homeowners |

| FHA Loan | 6.0% to 6.6% | First-time buyers with lower credit |

| VA Loan | 5.9% to 6.4% | Eligible veterans and service members |

These figures move daily with the broader bond market. Always confirm your quote directly with RoundPoint before you compare it against other lenders.

The ranges above come from a mix of recent industry averages and RoundPoint’s own origination history, not a live feed from the company. Think of them as a starting point for your conversation with a loan officer, not a guaranteed offer. Your actual number will always depend on your personal financial profile. Two borrowers applying on the same day can still receive different pricing based on credit and down payment alone.

How RoundPoint Rates Compare to the National Average

Industry origination data shows RoundPoint’s average 30-year fixed rate sits close to the national average, often within a tenth of a percentage point. In recent reporting, RoundPoint’s average landed near 6.62%, while the broader national average was about 6.55%. That is a small gap, which means RoundPoint tends to price in line with the rest of the market rather than well above or below it.

Closing costs tell a similar story. RoundPoint’s average fees have run lower than the national average for a 30-year fixed loan, making it a fairly low fee servicer overall. This matters because a slightly higher rate paired with lower fees can still save you money over the life of the loan. Always look at the full cost picture, not just the interest number.

This is a useful benchmark when you sit down with quotes from three or four different companies. A lender advertising a rate far below the national average is worth a second look, since it may come with extra points or hidden fees. RoundPoint’s pattern of pricing near the market average, paired with below average costs, tends to appeal to borrowers who want predictable, middle of the road terms rather than an aggressive teaser rate.

Factors That Affect Your RoundPoint Mortgage Rate

Several personal details shape the exact number RoundPoint offers you. Lenders look at your credit history, your down payment size, and your overall debt load together. Small changes in any one of these areas can move your rate up or down. Knowing what matters most helps you prepare before you apply.

Credit Score

Your credit score has the biggest single impact on the rate you get offered. Borrowers with scores above 740 usually qualify for the lowest available pricing. Scores in the 620 to 680 range still qualify for many loan types, but the rate will run higher. Paying down credit card balances before you apply can move your score enough to matter.

Even a jump of twenty points can shift you into a better pricing tier with most lenders, RoundPoint included. Pull your credit report at least sixty days before you apply so you have time to fix any errors. Late payments and high credit utilization tend to hurt your score the most.

Loan-to-Value Ratio

Your loan-to-value ratio compares your loan amount to your home’s value. A lower ratio, meaning a bigger down payment, usually earns a better rate. Borrowers who put down 20% or more often skip private mortgage insurance entirely. Even a 5% higher down payment can shift your final offer in a noticeable way.

Your debt-to-income ratio plays a supporting role as well. Lenders generally prefer this number to stay under 43%, though some loan programs allow more flexibility. Paying off a car loan or a large credit card balance before applying can lower this ratio quickly. A stronger overall financial profile almost always leads to a better rate offer.

RoundPoint Loan Options and Rate Types

RoundPoint prices its loans differently based on the program you choose. Each loan type carries its own risk profile, which shapes the rate you see. Picking the right option depends on your down payment, credit score, and how long you plan to stay in the home.

Fixed-Rate Mortgage

A fixed-rate mortgage locks your interest rate for the entire loan term. Your principal and interest payment never changes, even if market rates rise later. This option works well for buyers who plan to stay in their home for many years. Both 15-year and 30-year terms are available through RoundPoint, giving you flexibility to balance a lower monthly payment against a faster payoff timeline.

Adjustable-Rate Mortgage (ARM)

An adjustable-rate mortgage starts with a lower fixed rate for a set period, often five years. After that window, the rate adjusts based on market conditions. This can save money upfront for buyers who plan to sell or refinance before the adjustment period starts. It carries more long-term risk than a fixed loan, so most financial advisors recommend it only when you have a clear exit plan for your home.

FHA, VA, USDA and Jumbo Loans

RoundPoint also services government-backed loans, including FHA, VA, and USDA programs. FHA loans allow lower credit scores and smaller down payments, which makes them popular with first-time buyers. VA loans serve eligible veterans and active service members with no down payment required in most cases. Jumbo loans cover properties above conforming loan limits and usually carry slightly different pricing, since they fall outside standard Fannie Mae and Freddie Mac guidelines.

RoundPoint Refinance Rates

RoundPoint offers two main refinance paths: rate-and-term and cash-out. A rate-and-term refinance swaps your current loan for one with a better rate or shorter term, without pulling out extra cash. A cash-out refinance replaces your loan with a larger one and gives you the difference in cash, often used for renovations or debt consolidation.

Refinance rates typically run close to purchase rates but can shift slightly based on your current loan balance and equity position. If you already have a RoundPoint loan and want to check your current terms first, our RoundPoint Mortgage Login guide walks through account access step by step. Always request a written Loan Estimate before committing to any refinance offer.

Refinancing usually makes the most financial sense when you can lower your rate by at least half a percentage point, or when you need to remove private mortgage insurance. Run the numbers on your break-even point, which is how long it takes for your monthly savings to cover the closing costs. If you plan to move within a year or two, refinancing may not be worth the upfront expense.

RoundPoint Rate Lock Policy

A rate lock guarantees your interest rate for a set period while your loan closes. RoundPoint typically offers lock periods between 30 and 60 days, though longer locks may be available for a fee. Locking early protects you if market rates rise before closing, but it also means you will not benefit if rates drop.

Ask your loan officer about float-down options, which let you capture a lower rate if the market improves after you lock. Missing your closing deadline can force a costly relock at current market pricing. Confirm your lock expiration date in writing and track it closely.

Some lock periods come with a small fee, especially extended locks beyond 60 days. That fee is usually worth paying if you expect a slow closing process or a home under construction. Ask your loan officer to explain any lock fee in writing before you agree to it, so there are no surprises at the closing table.

Pros and Cons of RoundPoint Mortgage Rates

RoundPoint’s pricing tends to land close to the national average, and its fees often run lower than many competitors. The company also offers a wide range of loan types under one roof, from conventional to government-backed programs. That said, RoundPoint does not display live rates online, which forces extra phone calls just to get a basic quote. Weighing these points side by side helps you decide if the tradeoff is worth it for your situation.

- Competitive fees compared to the national average

- Wide range of loan and refinance options

- Established company with a long servicing history

- No published rates, so shopping takes more effort

- Customer service reports are mixed across review platforms

How to Get the Best Rate From RoundPoint

Start by checking your credit report for errors before you apply. Even small corrections can bump your score into a better pricing tier. Next, gather quotes from at least two other lenders so you have real numbers to compare against RoundPoint’s offer.

If you have questions about your current account or want a direct line to loan support, our RoundPoint Mortgage Phone Number guide lists the fastest contact options. You can also ask directly about discount points, which let you pay upfront cash for a lower long-term rate. For general RoundPoint mortgage questions, you can reach out to james@allthings-mortgage.com for extra guidance while you shop.

Timing also matters more than most borrowers realize. Rates can shift within the same week, so locking in during a favorable stretch protects your budget. Do not be afraid to ask your loan officer directly if the quoted number is their best offer, since some pricing has room to move for strong borrowers.

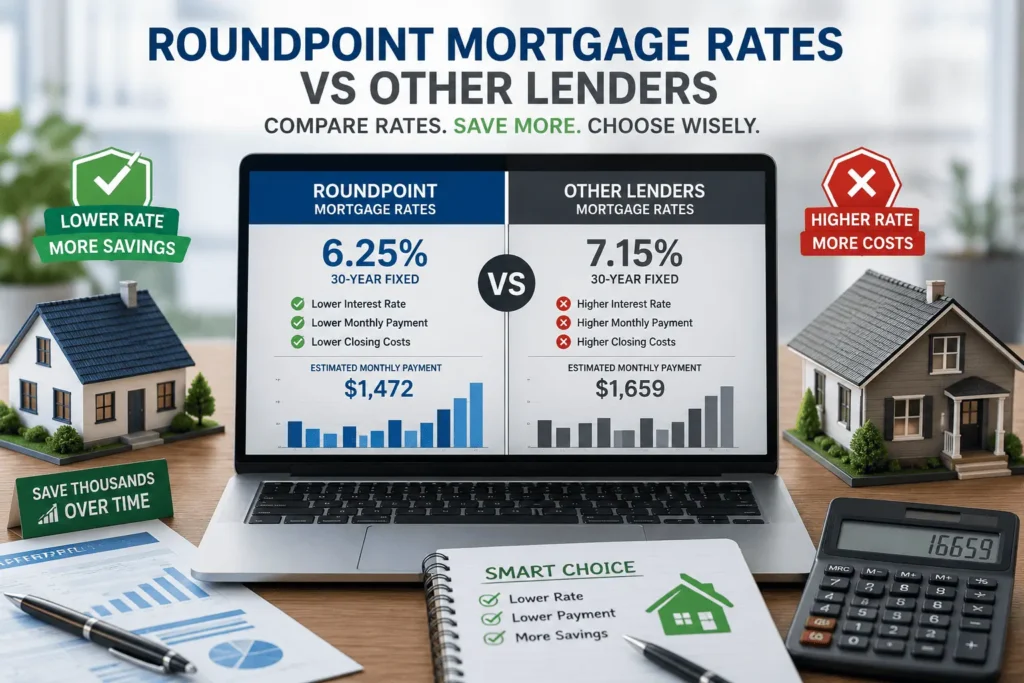

RoundPoint Mortgage Rates vs Other Lenders

Comparing RoundPoint against other national lenders helps you see where it stands on price and service. The table below lines up typical figures side by side.

| Lender | Typical Rate Range | Avg Fees | Min Credit Score |

|---|---|---|---|

| RoundPoint | 6.3% to 6.9% | Lower than average | 620 |

| Rocket Mortgage | 6.2% to 6.8% | Average | 620 |

| Better | 6.1% to 6.7% | Below average | 620 |

| PennyMac | 6.3% to 6.9% | Average | 580 |

RoundPoint holds its own on rate competitiveness, especially once you factor in its lower average closing costs. Lenders like Better and PennyMac may offer a fully digital process, so weigh convenience against your comfort with phone-based service. PennyMac’s lower minimum credit score requirement may appeal to borrowers who are still rebuilding their credit history. In the end, the right lender depends on your priorities, whether that is the lowest fees, the fastest closing, or the easiest online experience.

RoundPoint Fees and Closing Costs

RoundPoint’s average closing costs for a 30-year fixed loan have historically run below the national average. Typical costs include an origination fee, appraisal fee, title insurance, and prepaid escrow items. Ask for a full fee breakdown in your Loan Estimate so nothing surprises you at closing.

If your loan already transferred to RoundPoint and you want details on where payments go, our RoundPoint Mortgage Payment guide explains every payment method available. For questions about specific fee line items, james@allthings-mortgage.com can help point you toward the right documentation. Understanding these costs upfront keeps your total financial picture clear.

Remember that the annual percentage rate, or APR, gives you a more complete cost comparison than the interest rate alone. APR folds in most closing fees, so it shows the true yearly cost of borrowing. When you compare RoundPoint against another lender, always line up APR against APR rather than just the headline interest rate.

Conclusion

RoundPoint Mortgage Rates land close to the national average, with fees that often run a bit lower than competitors. As promised, you now have real rate ranges, a lender comparison, and clear steps to secure your best possible offer. Check your credit, gather outside quotes, and talk directly with a loan officer before you commit. That preparation is what turns a confusing rate search into a confident mortgage decision.

Frequently Asked Questions

What is RoundPoint’s current 30-year mortgage rate?

RoundPoint Mortgage Rates for a 30-year fixed loan typically range between 6.3% and 6.9%, depending on your credit score and down payment. Rates change daily with the broader bond market. Contact a loan officer directly for your personal quote, since RoundPoint does not post live pricing online.

Does RoundPoint publish its rates online?

No, RoundPoint does not display current mortgage rates on its public website. You need to start an application or call a loan officer to receive a personalized quote. This is different from many digital-first lenders that show sample rates upfront for easy comparison.

Is RoundPoint a good mortgage lender?

RoundPoint offers competitive pricing and lower than average fees, making it a solid option for many borrowers. Its main drawback is the lack of published rates, which adds extra steps to the shopping process. Reading recent customer reviews can help you decide if it fits your needs.

How do I lock in a rate with RoundPoint?

You can lock your rate through your assigned loan officer once your application is underway. RoundPoint typically offers 30 to 60 day lock periods, with longer options available for a fee. Ask about float-down features if you want protection against rising rates.

What credit score do I need for RoundPoint’s best rate?

Borrowers with credit scores above 740 usually qualify for RoundPoint’s lowest available pricing. Scores between 620 and 680 can still qualify for many loan programs, though the rate will be higher. Improving your score before applying can meaningfully lower your offer.