Imagine locking in a 3% mortgage rate during the pandemic and then needing to move a few years later. Current rates are sitting near 6.5%, and giving up that low rate feels like throwing money away every single month. Millions of homeowners are stuck in this exact situation right now, and it is one of the biggest reasons the housing market has slowed down so much. If you have ever wondered how would a portable mortgage work and whether it could save you from this rate trap, you are in the right place.

This article breaks down everything about portable mortgages — how the process works step by step, what happens when you buy a more or less expensive home, how much money you could actually save, and why this option does not exist in the United States yet. By the end, you will have a clear picture of whether porting a mortgage is a real solution for your situation or not.

What Is a Portable Mortgage?

A portable mortgage lets you transfer your existing mortgage — including the interest rate, remaining balance, and loan terms — from your current home to a new one. Instead of paying off your loan when you sell and starting over at today’s higher rates, you carry the original mortgage over to the next property.

Think of it like moving your mortgage the same way you move your furniture. The debt follows you rather than staying tied to the old house. Your lender releases the mortgage from the sold property and registers it against the new one.

The core benefit is simple. If you locked in a low rate years ago, you keep that rate on the ported balance. You do not reset. You do not refinance. The original loan structure stays intact as long as you meet your lender’s approval requirements.

How Does a Portable Mortgage Work Step by Step?

The process is more structured than most people expect. It is not as simple as just telling your lender you are moving. Each step requires action from both the borrower and the lender.

Notify Your Lender and Request the Port

The first step is contacting your lender as early as possible once you decide to move. You formally request to port the mortgage to a new property. Most lenders require this request within a set window — often 30 to 90 days from when you sell your current home. Missing this window means losing the right to port entirely.

New Property Appraisal and Lender Approval

Your lender does not automatically approve every new property. The new home must meet certain standards. It typically needs to be a residential property in the same country, and the lender will order an appraisal to confirm its value. If the property does not qualify — for example, it is a commercial property or does not meet minimum value thresholds — the port gets denied.

Borrower Requalification — Credit, Income, and DTI Check

This is the step most people do not expect. Even though you already have the mortgage, you must requalify as a borrower. The lender reviews your current credit score, income, employment status, and debt-to-income ratio. If your financial situation has gotten worse since the original loan, the lender can deny the port even if the property qualifies. You need to be in the same or a better financial position than when you first got the mortgage.

Old Mortgage Discharged and Registered on New Property

Once the lender approves both the property and the borrower, the legal transfer happens. The mortgage is discharged from the old property and registered against the new one. If there is a gap between your ported balance and the new home’s purchase price, that gap gets handled separately through additional financing at current market rates.

What Happens When the New Home Costs More or Less?

The price difference between your old home and new home changes how porting plays out. There are three scenarios and each one works differently.

Upsizing — How Gap Financing Works at Current Rates

If your new home costs more than your remaining mortgage balance, you need to cover the difference. Say you have $250,000 left on your mortgage at 3% and the new home costs $400,000. You port the $250,000 at 3% and take a separate loan for the remaining $150,000 at today’s rate — currently around 6.5%. This is called a blend-and-extend or gap loan arrangement. Your monthly payment reflects two rates: the low ported rate on the original balance and the higher current rate on the extra amount.

Downsizing — What Happens to Your Remaining Balance

If the new home costs less than your remaining mortgage balance, the situation gets more complicated. You cannot simply carry over more mortgage debt than the property is worth. Most lenders require you to pay down the excess balance before completing the port. In some cases, you may be able to carry the excess as a second loan, but this depends entirely on the lender’s policies. Downsizing with a portable mortgage requires a direct conversation with your lender well before you list your home.

| Scenario | Ported Balance | Extra Financing | Rate Impact |

|---|---|---|---|

| Upsizing | Full remaining balance | Gap loan at current rate | Blended rate on total payment |

| Same Price | Full remaining balance | None needed | Original low rate maintained |

| Downsizing | Reduced to match new value | Possible paydown required | Low rate on reduced balance |

Portable Mortgage vs Refinancing — Which Saves You More Money?

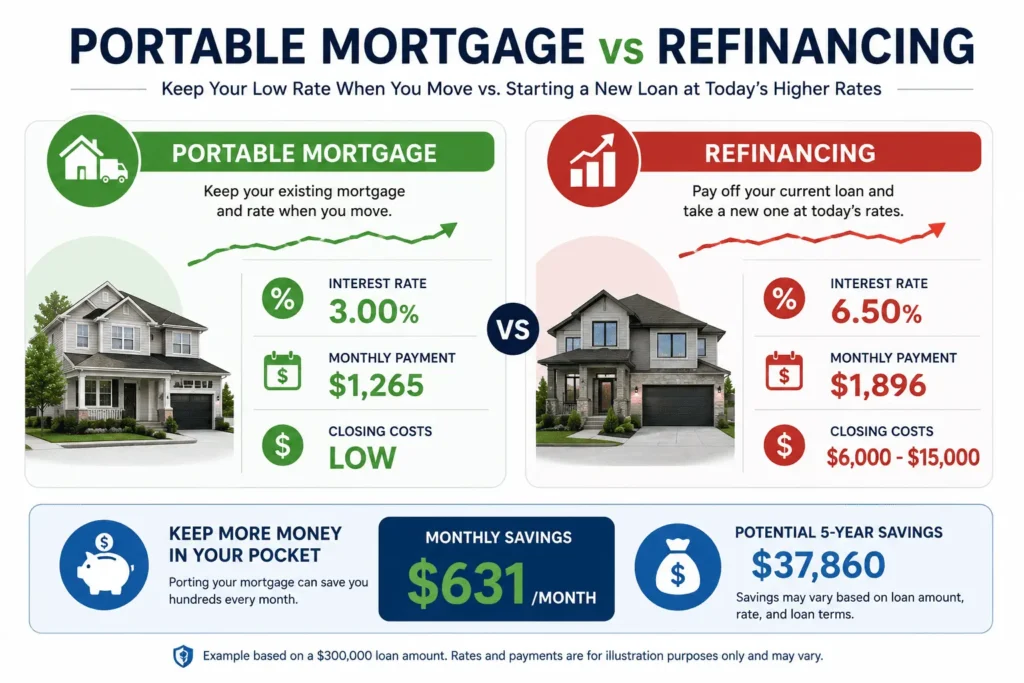

When you refinance, you pay off your existing loan and take a brand new one at current rates. When you port, you keep the old rate on the existing balance. The difference in cost between these two paths can be significant over time.

On a $300,000 balance, a 3% rate gives you a monthly principal and interest payment of roughly $1,265. The same balance at 6.5% brings that payment to around $1,896. That is a difference of $631 every single month. Over five years, porting instead of refinancing saves approximately $37,860 on that balance alone.

Refinancing also comes with closing costs — typically 2% to 5% of the loan amount. On a $300,000 loan that is another $6,000 to $15,000 out of pocket. Porting generally avoids most of these costs, though your lender may charge a portability fee. For most borrowers with a significant rate gap, porting wins clearly over refinancing. You can review how recasting a mortgage compares as another alternative for managing your existing loan terms.

How Much Can You Save With a Portable Mortgage?

The actual savings depend on three things: the size of your ported balance, the gap between your original rate and current rates, and how long you stay in the new home.

Here is a real-number breakdown using a $300,000 ported balance at 3% versus taking a new loan at 6.5%:

- Monthly savings: $631 per month

- 1-year savings: $7,572

- 5-year savings: $37,860

- 10-year savings: $75,720

These numbers only cover the ported balance. If you need gap financing for a more expensive home, those savings get partially offset by the higher rate on the additional amount. But even with a $100,000 gap loan at 6.5%, the net savings over five years on a $300,000 ported balance remain well above $25,000 for most borrowers.

Who Should Use a Portable Mortgage and Who Should Not?

Portable mortgages are not the right move for every homeowner. The benefit depends almost entirely on how big the gap is between your existing rate and current market rates.

Best candidates for porting:

- Homeowners who locked in rates between 2% and 4% before 2023

- Move-up buyers who need more space but want to keep their payment manageable

- Long-term owners with strong equity in their current home

- Borrowers whose income and credit have remained stable or improved

Porting will not help you if:

- You are a first-time buyer with no existing mortgage

- Your current rate is only slightly below today’s rates

- Your financial situation has declined since you got the original loan

- You have very little time left on your mortgage term

The closer your current rate is to today’s market rate, the smaller the benefit. If you are at 5.5% and current rates are 6.5%, the monthly savings barely justify the effort and paperwork involved.

Prepayment Penalties and Porting — What You Need to Know

This is one of the most overlooked parts of mortgage portability. In countries where portable mortgages exist, breaking your mortgage to move — without porting — usually triggers a prepayment penalty. These penalties can be substantial, sometimes running into thousands of dollars depending on the loan size and remaining term.

Porting the mortgage avoids this penalty entirely because you are not technically breaking the loan. You are transferring it. For homeowners in Canada or the UK, this penalty avoidance alone can make porting the financially smarter choice even when the rate difference is modest.

Fixed-rate mortgages generally carry higher prepayment penalties than variable-rate mortgages. If you have a fixed-rate loan and are considering moving, calculating the penalty cost versus the savings from porting should be one of your first steps before making any decision.

Tax Implications of Porting a Mortgage

Porting a mortgage does not create a taxable event on its own. Transferring the loan from one property to another is a financing transaction, not a sale of an asset. The IRS — or its equivalent in other countries — does not treat the port itself as income or a gain.

However, selling your current home may trigger capital gains tax depending on how much the property has appreciated and how long you have lived there. In the United States, the current exclusion allows up to $250,000 in gains for single filers and $500,000 for married couples filing jointly if the home was your primary residence for at least two of the last five years.

The interest deductibility question also matters. If you port your original mortgage and add a gap loan, the interest on both portions may be deductible — but the rules depend on how the loans are structured and what the funds are used for. Consulting a tax professional before completing a port is always the right move.

Is a Portable Mortgage Available in the United States Right Now?

The short answer is no. Portable mortgages are not currently available in the United States. But the conversation around them has moved further than ever before, and real policy discussions are happening at the federal level.

Current FHFA Status and What Has Been Proposed

In late 2025, Federal Housing Finance Agency Director Bill Pulte confirmed publicly that the agency is actively evaluating portable mortgages as a policy option. The FHFA oversees Fannie Mae and Freddie Mac, which together back the majority of U.S. mortgages. Any portable mortgage system in the U.S. would require their involvement. As of early 2026, no formal proposal has been passed, but the evaluation is ongoing and the political interest is real.

The Mortgage-Backed Securities Problem Blocking Portability

The biggest structural barrier is how U.S. mortgages are funded. Most American home loans are packaged and sold to investors as mortgage-backed securities. Those investors buy into specific loan terms tied to specific properties. Allowing a borrower to transfer a loan to a new property disrupts the cash flow assumptions those investors made when they bought the securities. This creates pricing uncertainty and potential losses for MBS investors, which is why lenders and economists have serious concerns about implementing portability within the current U.S. mortgage finance system.

How Canada and the UK Made Portable Mortgages Work

Both Canada and the UK operate mortgage systems where banks often hold loans directly on their books rather than selling them into a secondary market. Canadian mortgages also run on shorter fixed terms — typically five years — which makes the math easier to manage when a loan moves to a new property. These structural differences are exactly why portability works there and why copying their model directly into the U.S. system is not straightforward.

When Porting Makes Sense and When a New Loan Is the Better Choice

Choosing between porting and getting a new loan comes down to one thing — how much money you actually save after accounting for all the costs involved. The rate gap, your new home’s price, your financial situation, and your lender’s approval all play a role. Running the numbers before you decide is not optional, it is essential.

Strong Signs You Should Port Your Mortgage

- Your current rate is at least 1.5% to 2% below today’s market rate

- You plan to stay in the new home for at least three to five years

- Your income and credit score have stayed stable or improved

- The new home is close in price to your current mortgage balance

- You want to avoid prepayment penalties on a fixed-rate loan

Clear Signs You Should Get a New Loan Instead

- Your current rate is close to today’s rates and the savings are minimal

- You need significantly more financing and the blended rate closes the gap

- Your lender does not offer portability or denies your application

- You are moving to a property type the lender will not approve for porting

- Your financial situation has weakened since the original loan was issued

Conclusion

Understanding how would a portable mortgage work is more relevant today than it has ever been, with millions of homeowners locked into low rates and hesitant to move. This article walked you through the full process — from the step-by-step transfer mechanics to gap financing, savings calculations, tax considerations, and the real barriers keeping this option out of the U.S. market. Porting is not available to American homeowners yet, but the policy conversation is moving forward and the financial case for it is strong. If and when portable mortgages arrive in the U.S., the homeowners who understand how they work will be the ones ready to take full advantage.

Frequently Asked Question

Does Arvest Publish Its Mortgage Rates Online?

Arvest Central Mortgage posts daily sample rates for conventional, FHA, and VA loans on its website. The main Arvest Bank site requires a ZIP code entry or direct loan officer contact for location-specific pricing. Rates change every business day so any posted figure is a reference point, not a guaranteed quote.

What Credit Score Do You Need for an Arvest Mortgage?

Conventional loans require a minimum credit score of 620. FHA loans accept scores as low as 580 with 3.5% down. VA and USDA loans have more flexible credit requirements. Your score directly affects the rate you are offered.

What Is the Minimum Down Payment at Arvest?

Conventional loans start as low as 3% down. FHA loans require 3.5% with a 580 credit score. VA and USDA loans allow zero down payment for qualified borrowers. Putting less than 20% down on a conventional loan triggers private mortgage insurance.

How Do You Lock Your Rate With Arvest?

Once you agree on loan terms with your Arvest loan officer, you sign a rate-lock agreement that freezes your rate for up to 45 days. Rates move daily so locking early protects you from market increases before your closing date.

Does Arvest Service Its Own Mortgage Loans?

Yes. Arvest services 99% of the loans it originates, meaning your loan stays with Arvest after closing. You will not be transferred to an unknown third-party servicer. This gives borrowers consistent support and a single point of contact throughout the loan term.