Millions of homeowners locked in a cheap mortgage a few years ago. Now many of them want to move but feel stuck. Selling means giving up a 3% deal and taking a new one above 6%. That trade can add hundreds of dollars to a monthly payment.

This is where portable mortgage rates enter the picture. The idea lets you carry your current deal to your next house instead of starting over. In this guide, you will learn how porting works, what it costs, who qualifies, and whether it is coming to the United States. By the end, you will know exactly what this option could mean for your next move.

What Is a Portable Mortgage Rate?

A portable mortgage rate is an interest rate that moves with you when you sell one house and buy another. Instead of paying off your old loan and opening a new one, your existing balance, term, and pricing transfer to the new property. You keep the deal you already have.

This setup is common in Canada and the United Kingdom. It is not offered in the United States right now. You can read more about how a portable mortgage is structured if the concept is new to you.

The main appeal is simple. If your current pricing is far below what lenders charge today, porting protects that advantage. You avoid resetting your borrowing cost at a worse level.

How Porting a Mortgage Rate Works

Porting starts when you sell your current place and buy another one at the same time. Your lender reviews your finances again and checks the new property. If everything passes, your balance and terms move over. Most lenders give you a set window to complete both deals.

The process changes based on the price of your next house. There are two main paths. We cover how a portable mortgage would work in more detail in a separate guide.

Moving to a Home of Equal or Lower Value

This is the easiest case. Your remaining balance simply attaches to the new property. Your payment, term, and pricing stay the same.

One caution applies when you downsize. If the new place costs much less, you may pay down a big chunk of your balance at once. Some lenders charge a fee if you prepay more than their yearly limit. Ask about this before you sell.

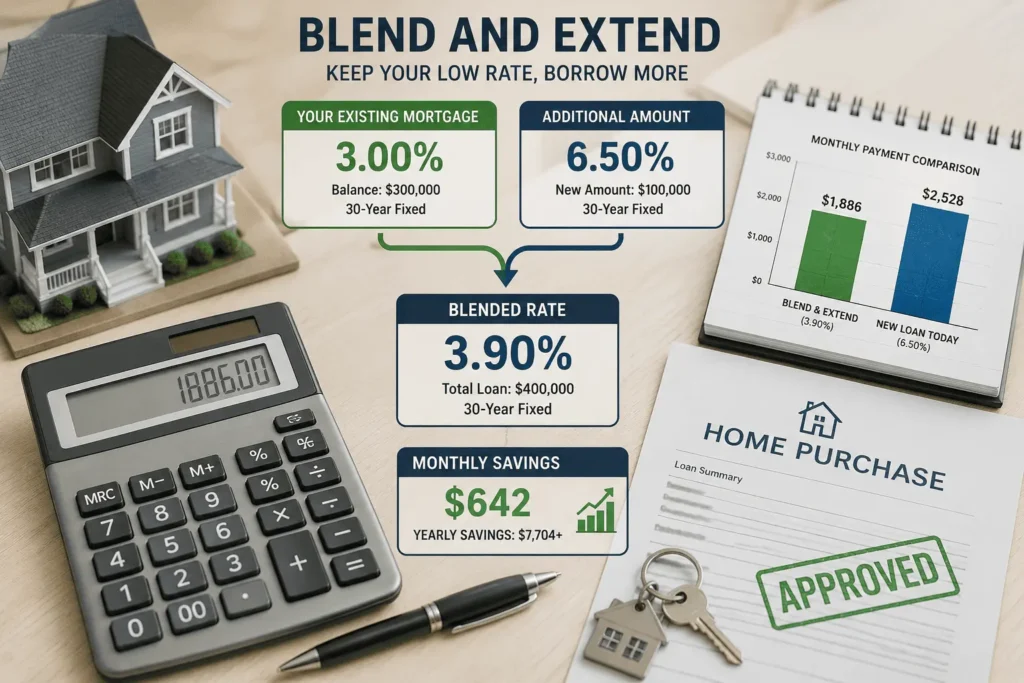

Moving to a More Expensive Home: Blend and Extend Rates

Most people move up, not down. If the new house costs more than your balance, you need extra money. Lenders handle this with a method called blend and extend. Your old pricing covers the original balance, and the new funds are priced at today’s level.

The two amounts are mixed into one weighted figure. Here is a simple example. Say you owe $300,000 at 3% and need $100,000 more at 6.5%. Your blended figure lands near 3.9%, which beats taking the full $400,000 at today’s pricing.

| Option | Amount | Pricing | Monthly Payment (30 yr) |

|---|---|---|---|

| Ported with blend and extend | $400,000 | ~3.9% | ~$1,886 |

| Brand new loan today | $400,000 | 6.5% | ~$2,528 |

| Monthly savings | ~$642 |

That gap adds up to more than $7,700 every year. A portability calculator from your lender can run these numbers for your exact balance. Always compare both paths before you commit. Keep porting fees in mind as well. Lenders may charge an administration fee, and you still pay normal closing costs like appraisal and legal charges. These costs are usually small compared to the savings shown above. Still, add them to your math so the final number is honest.

Are Portable Mortgage Rates Coming to the United States?

The idea gained national attention in late 2025. The Federal Housing Finance Agency said it is actively evaluating portability for American borrowers. The agency oversees Fannie Mae and Freddie Mac, which back more than half of US home financing. Officials see porting as a way to fix the lock-in effect.

The lock-in effect is real. More than half of American homeowners with a mortgage hold pricing below 4%. Average levels today sit above 6%. Many families refuse to sell because moving would nearly double their borrowing cost.

Critics raise a serious concern, though. American home loans are bundled into mortgage-backed securities and sold to investors. Those investors price the bonds based on the property tied to each loan. If the property can change midstream, the risk models break.

Experts warn this disruption could push borrowing costs higher for everyone. Investors would demand extra return to cover the new uncertainty. So a fix meant to help movers might raise prices for first-time buyers. Nothing is final yet, and no official program exists today.

Would a Portable Mortgage Rate Be Higher Than a Regular Rate?

Probably yes, at least a little. Housing economists expect lenders to charge a small premium for the porting feature. The extra cost would offset the added risk that investors take on. Think of it like paying slightly more for a flexible airline ticket.

Estimates suggest the premium would be modest, not massive. A borrower might pay a bit more upfront in exchange for protection later. If market pricing jumps after you buy, that protection becomes very valuable. If pricing falls instead, you paid for a feature you never used.

This trade-off matters for anyone comparing offers. A slightly higher figure today could save you thousands when you move during an expensive market. Your time horizon decides whether the math works in your favor. There is one more angle worth knowing. Regulators are also studying a 50-year term and assumption changes as part of the same affordability push. If several tools launch together, lenders will compete harder on pricing. That competition could shrink any premium over time.

Portable Mortgage Rates in Canada and the UK

Canada and the UK have offered porting for decades. Their systems make it easier because fixed terms are short. A Canadian borrower usually locks pricing for five years or less. That short window limits the risk lenders carry.

Canadian lenders typically give borrowers 30 to 120 days to complete a port. You must sell and buy within that window. Banks also require you to qualify again under current rules. Your income, debts, and credit all get a fresh review.

The UK works in a similar way. Porting there is a standard feature on many products, not a special request. Borrowers use it to avoid early repayment charges when they move mid-term. These markets prove the concept can run smoothly under the right structure. Some Canadian lenders also offer a port and hold option. This protects your terms for a short period if your purchase closes after your sale. It gives families breathing room when the two deals do not line up perfectly. Ask your lender if this safety net is part of your contract.

Who Qualifies to Port a Mortgage Rate?

Porting is never automatic. Lenders treat it like a new application with one big perk attached. You must show that your finances still support the debt. People whose income dropped or whose debts grew can be denied.

The property matters too. Lenders check that the new house fits their standards and lending area. Unusual properties like raw land or some condos may not qualify. Timing is the final piece, since your sale and purchase must close within the allowed window.

Here is what lenders usually review:

- Current income and job stability

- Credit history since the original approval

- Total monthly debts compared to earnings

- The value and condition of the new property

- Whether your product includes a porting feature at all

Steps to Port Your Mortgage Rate

- Call your lender and confirm your product allows porting.

- Get pre-approved again under current qualification rules.

- List your home and shop for the new one at the same time.

- Line up both closing dates inside the porting window.

- Sign the transfer paperwork and carry your terms to the new address.

Following these steps in order prevents the most common failure, which is missing the deadline. A good broker can keep both deals on schedule.

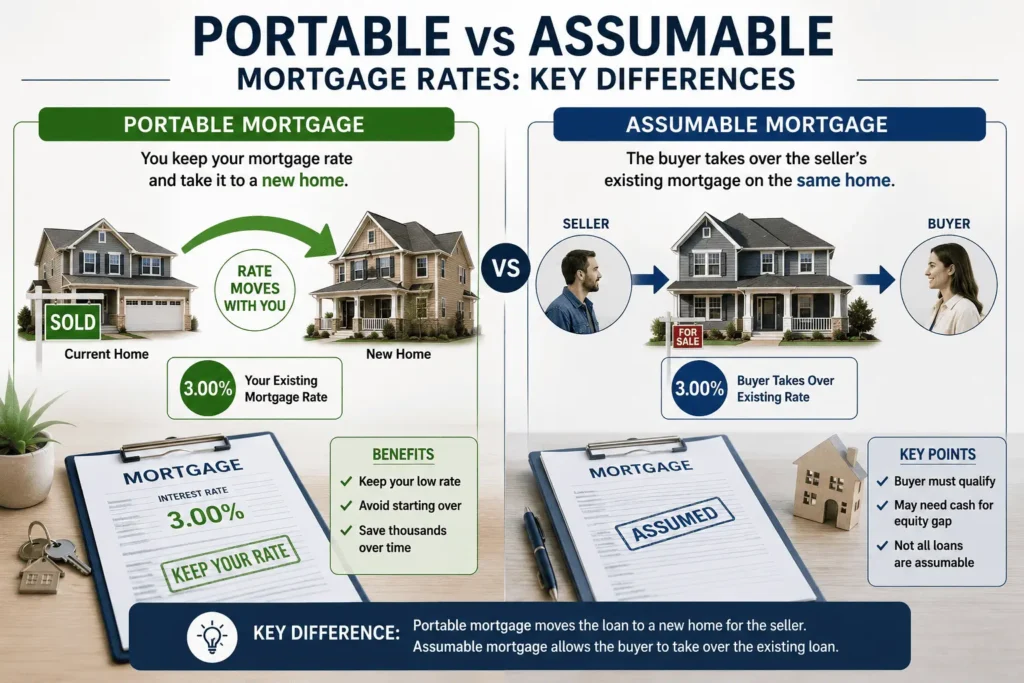

Portable vs Assumable Mortgage Rates: Key Differences

People often mix up these two options, but they work in opposite directions. Porting lets the seller keep their own deal and take it to their next house. Assumption lets the buyer take over the seller’s existing deal on the same house. The benefit moves with a different person in each case.

Assumable financing already exists in the United States. Government-backed products like FHA, VA, and USDA loans allow assumption when the buyer qualifies. Most conventional products do not. The buyer must also cover the seller’s equity, often with cash or a second loan.

Porting has no legal home in America yet. So today, assumption is the only realistic way for a US buyer to grab someone’s old low pricing. If regulators approve portability later, sellers would finally get a matching tool. Knowing who offers mortgages with an assumption feature can help buyers hunt for these deals now.

Pros and Cons of Porting Your Mortgage Rate

Porting sounds great, but it has real limits. Weigh both sides before building your moving plan around it.

Benefits:

- You keep below-market pricing when you move

- You skip prepayment penalties that can cost thousands

- Blend and extend lets you borrow more without losing your old deal

- Your amortization schedule keeps moving forward without a reset

Drawbacks:

- You must qualify all over again, and approval is not guaranteed

- Tight 30 to 120 day windows create stressful timing pressure

- Blended pricing is always higher than your original figure

- Administrative fees, appraisals, and legal costs still apply

- Variable products often cannot be ported at all

For many movers, the savings crush the costs. For others, especially those whose finances changed, breaking the contract may be the only path.

Alternatives to Portable Mortgage Rates

American borrowers cannot port today, but other tools can soften the blow of moving. Each one attacks the affordability problem from a different angle.

An assumable loan is the closest cousin. Buyers can search for sellers with government-backed financing and take over their terms. A temporary buydown is another route, since sellers sometimes fund a lower payment for the first one to three years. This option works well for first-time homebuyers who expect their income to grow.

Refinancing later is a patient strategy. You accept today’s pricing, then refinance when the market drops. A bridge loan helps with timing instead of cost, letting you buy before you sell. Talk to lenders about which mix fits your situation, or email james@allthings-mortgage.com for guidance on your options.

Conclusion

At the start, we promised to explain how this option works, what it costs, and whether you can use it. We covered the porting process, blend and extend math, qualification rules, and the US proposal debate. Right now, portable mortgage rates remain a Canadian and British tool, while American borrowers wait on regulators. Keep an eye on FHFA announcements, because rate portability could reshape how Americans move in the years ahead.

Frequently Asked Questions

Can you transfer your mortgage rate to a new house?

Only if your loan includes a portability feature. Borrowers in Canada and the UK can transfer their balance, term, and pricing to a new property. American borrowers cannot do this yet because no US lender currently offers the feature.

Are portable mortgages legal in the US?

No law bans them, but the American securitization system makes them impractical. The Federal Housing Finance Agency is studying the idea as of 2026. Until regulators and investors solve the bond pricing problem, no official program exists for US borrowers.

How long do you have to port a mortgage?

Most lenders allow 30 to 120 days between selling your old home and closing on the new one. The exact window depends on your lender and product. Missing the deadline cancels the port and may trigger prepayment penalties.

Can you port a variable-rate mortgage?

Usually not directly. Most lenders require you to convert a variable product into a fixed one before porting. Some lenders refuse to port variable products at all. Check your contract terms early so the rule does not surprise you mid-move.

What is a blend and extend mortgage rate?

It is a weighted mix of your old pricing and current market pricing. Lenders use it when you port and need extra funds for a costlier house. The blended figure sits between the two levels, saving you money versus a full new loan.