Millions of homeowners feel stuck in their houses right now. Maybe you are one of them. You locked in a 3% rate a few years ago, and now you want to move. But giving up that rate for a 6% loan feels like throwing money away. So you stay put, even when your home no longer fits your life.

The good news is that Washington has noticed this problem. The portable mortgage trump proposal could let you carry your low rate to your next home. In this guide, we will break down what this idea means, how it would work, who would qualify, and what you can do today. By the end, you will know exactly where things stand and how to plan your next move.

What Is a Portable Mortgage?

A portable mortgage is a home loan that moves with you. When you sell your house and buy a new one, you keep your current interest rate, loan balance, and term. You do not need to apply for a brand new loan at today’s higher cost.

This is very different from how American home loans work now. Today, when you sell your home, your loan gets paid off from the sale. Then you start fresh with a new loan on the next property. Portability breaks that old pattern and puts the loan in your hands, not the house.

Why Is the Trump Administration Considering Portable Mortgages?

The idea gained national attention in late 2025. Bill Pulte, the Director of the Federal Housing Finance Agency (FHFA), posted on X that his agency was “actively evaluating” portable home loans. He said Fannie Mae and Freddie Mac were looking at how to offer them in a safe and sound way.

This came right after President Trump floated the idea of 50-year home loans. The White House has been testing several ideas to fix housing affordability. The administration mortgages push also included a $200 billion mortgage bond purchase plan through Fannie Mae and Freddie Mac. All these moves target one big issue, and that issue is the lock-in effect.

The Mortgage Lock-In Effect Explained

The lock-in effect is simple to understand. Redfin found that 52.5% of American homeowners have a rate below 4%, based on FHFA data. Today’s average 30-year fixed rate sits above 6%. So moving means trading a cheap loan for an expensive one.

Picture a family paying $1,500 a month on their current loan. The same loan amount at today’s rates could cost them $500 more every month. That math keeps sellers off the market. Fewer sellers means fewer homes for buyers, and the whole housing market freezes up.

How Would a Portable Mortgage Work?

The basic process is easy to picture. You sell your home, buy a new one, and your lender transfers your existing loan to the new property. Your rate, your remaining balance, and your payoff timeline all stay the same. You can read a full breakdown of how a portable mortgage would work step by step.

The details change based on the price of your next home. Let’s look at both situations.

Porting to a Cheaper Home

This is the simple case. Say you owe $250,000 on your current loan at 3%. You sell your home and buy a smaller one for $230,000. The money from your sale pays down part of your balance.

Your loan simply shrinks to fit the new home. Your rate never changes, and your monthly payment drops. This setup works well for retirees who want to downsize. It also helps empty nesters who no longer need extra space.

Porting to a More Expensive Home

This case gets trickier. Say you owe $250,000 at 3%, but your new home costs $300,000. Your old loan only covers part of the price. You must fill that $50,000 gap somehow.

You have two main choices here. You can pay the difference in cash from your savings or sale profits. Or you can take a second loan for the gap at current market pricing. Your blended monthly cost would still beat a full new loan at today’s portable mortgage rates and terms.

Would Your Current Mortgage Qualify for Porting?

This is the question everyone wants answered. Sadly, the honest answer is probably not. Most experts believe portability would only apply to new loans written after a rule change. Your existing loan contract does not include a porting feature.

Here is why this matters so much. Investors already bought your loan as part of a bundle. Changing its terms now would break the deal those investors agreed to. Housing analysts have repeatedly warned that retroactive porting is almost impossible under current contracts. So if this plan becomes real, it would likely help future borrowers, not current ones.

Why the US Doesn’t Have Portable Mortgages Like Canada and the UK

Porting is normal in Canada and the United Kingdom. Borrowers there move their loans between homes all the time. But their systems are built very differently from ours. Canadian and British loans usually run on short terms of two to five years.

After those short terms end, borrowers renew and renegotiate their loans. Lenders never promise one rate for 30 years. That short cycle makes porting easy to manage. American borrowers lock in fixed rates for 15 or 30 years, which is a much bigger promise to keep.

There is also the money machine behind US lending. American home loans get bundled into mortgage-backed securities and sold to investors. Each loan in a bundle is tied to one specific property. Moving a loan to a new house would scramble how these bundles get priced, and that could push borrowing costs higher for everyone.

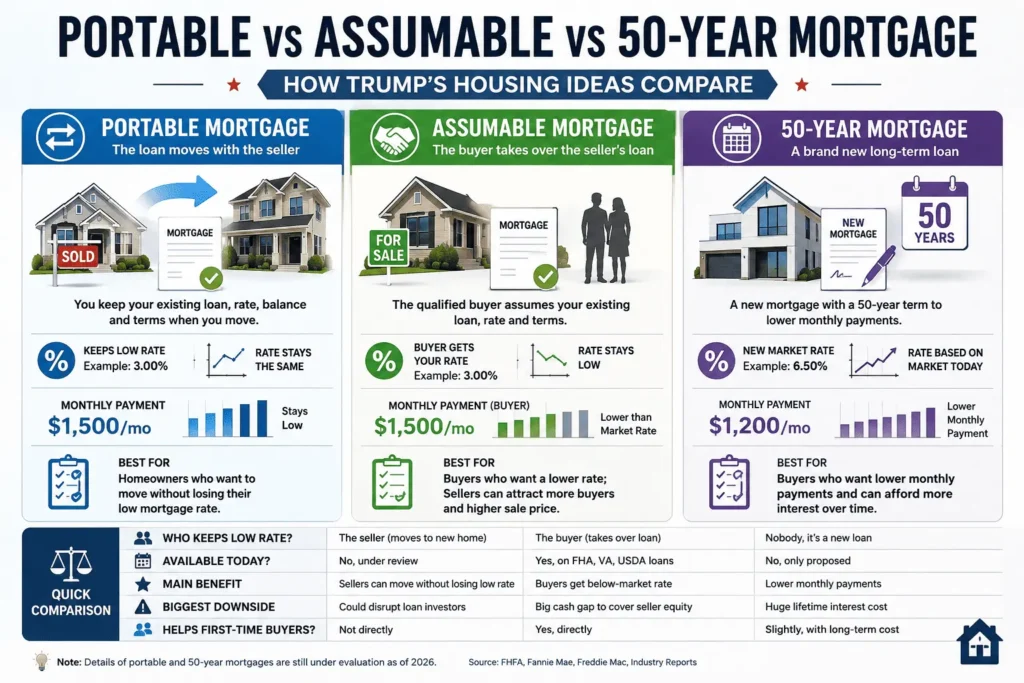

Portable vs Assumable vs 50-Year Mortgage: How Trump’s Housing Ideas Compare

The White House floated three big housing ideas in late 2025. People often mix them up, but they work in very different ways. The trumps plan discussions covered all three options at once. Here is how they stack up side by side.

| Feature | Portable Mortgage | Assumable Mortgage | 50-Year Mortgage |

|---|---|---|---|

| Who keeps the low rate | The seller takes it to a new home | The buyer takes over the seller’s loan | Nobody, it’s a new loan |

| Available today | No, still under review | Yes, on FHA, VA, and USDA loans | No, only proposed |

| Main benefit | Sellers can move freely | Buyers get below-market pricing | Lower monthly payments |

| Biggest downside | Could disrupt loan investors | Big cash gap to cover seller equity | Huge lifetime interest cost |

| Helps first-time buyers | Not directly | Yes, directly | Slightly, with long-term cost |

As you can see, each option serves a different person. Portability helps current owners, assumptions help buyers, and the 50-year idea mainly lowers monthly bills.

Potential Benefits of Portable Mortgages

Supporters believe porting could shake the housing market loose. Susan Wachter, a real estate professor at the Wharton School, told CNN that portability could push hesitant owners to finally sell. That would open doors for waiting buyers. Here are the main benefits experts point to:

- You keep your low rate, so moving no longer punishes you with a higher monthly payment for the same loan amount.

- Housing inventory opens up, because locked-in sellers finally list their homes and give buyers more choices.

- Lifetime interest savings stay protected, since a 3% loan saves you tens of thousands compared to a 6% loan.

- Job and family moves get easier, because you can relocate for work or loved ones without a financial penalty.

- Closing costs may shrink, since transferring a loan could involve less paperwork than starting from zero.

Risks and Expert Concerns

Not everyone is cheering for this idea. Many housing economists see serious problems hiding under the surface. Their warnings deserve a fair look before anyone celebrates.

Could Home Prices Jump Even Higher?

More buying power often means higher prices. Kevin Thompson, CEO of 9i Capital Group, told Newsweek that demand would jump overnight if people could carry low rates with them. Prices would move higher with no question, in his view.

We saw this pattern during the pandemic boom. Cheap borrowing pushed home values up at record speed. Portability could repeat that story. The plan might fix mobility while making affordability even worse.

Little Relief for First-Time Buyers and Renters

Here is the fairness problem. Porting only rewards people who already own homes with low rates. Renters and first-time buyers get nothing from this feature. They would still face today’s high rates and high prices.

Some economists worry this widens the wealth gap. Existing owners gain a golden ticket they can use for decades. New buyers compete against them with weaker financing. Critics say any real fix must help people enter the market, not just move within it.

Is the Portable Mortgage Proposal Approved Yet? (2026 Update)

No, the proposal has not been approved as of mid-2026. The FHFA is still in the evaluation stage. No formal rules, timelines, or program details have been released. Pulte has continued rolling out other housing changes, like easing insurance requirements and approving new credit score models.

Donald Trump has kept housing costs in the spotlight throughout 2026. But the donald mortgages porting idea remains just that, an idea. Industry watchers note that rebuilding the securities system would take years, not months. Anyone making moving plans should treat portability as a maybe, not a promise.

What Homeowners and Buyers Can Do Right Now

You do not have to wait on Washington to make smart moves. Several real options exist today that capture some of the same value. If you have questions about your specific situation, you can reach out at james@allthings-mortgage.com for guidance.

Start by checking if your loan is assumable. FHA, VA, and USDA loans already allow qualified buyers to take over your terms. That feature can make your home more attractive to buyers and may even boost your sale price. Sellers with these loans hold a real edge in today’s market.

Buyers can ask sellers for a temporary rate buydown, which lowers payments for the first few years. Current owners with extra cash can request a recast, which shrinks the monthly payment without touching the rate. And if you must buy now at a high rate, plan to refinance later when rates fall. These steps keep you moving while the porting debate plays out.

Conclusion

We promised to explain where this proposal stands, and now you have the full picture. The portable mortgage trump idea could free millions of locked-in owners, but it remains under review with no approval, no timeline, and likely no benefit for existing loans. The smart play today is using real tools like assumable loans, buydowns, and recasting while watching the FHFA’s next steps. Keep your plans flexible, because housing policy can shift fast in the months ahead.

Frequently Asked Questions

Did Trump approve portable mortgages?

No, portable home loans have not been approved. The FHFA under Director Bill Pulte said it is actively evaluating the idea. As of mid-2026, no formal program, rules, or launch date exist. It remains only a proposal under government review.

Can I transfer my mortgage rate to a new house right now?

No, American home loans cannot be transferred between properties today. Your loan must be paid off when you sell. The only similar option is an assumable loan, where a qualified buyer takes over your existing FHA, VA, or USDA loan.

What is the difference between a portable and assumable mortgage?

A portable loan moves with the seller to their next home, keeping the same rate and balance. An assumable loan stays on the property, letting the buyer take over the seller’s terms. Portability helps sellers, while assumption helps buyers directly.

When will portable mortgages be available in the US?

There is no confirmed date. The FHFA is still studying feasibility, and rebuilding the mortgage-backed securities system could take years. Experts suggest any program would apply to new loans only. Borrowers should not delay plans waiting for this feature.

Will portable mortgages lower home prices?

Probably not, and prices could actually rise. Economists warn that letting owners keep low rates would boost buying power and demand quickly. More demand usually pushes prices higher. The feature improves mobility but does not directly fix housing affordability problems.

Do portable mortgages exist in Canada?

Yes, porting is common in Canada and the United Kingdom. Borrowers there can move loans between homes because their terms run only two to five years. Short renewal cycles make porting easy, unlike America’s 30-year fixed-rate loan structure.